It is for all these reasons--to protect against risk; to eliminate debt; you're going to live a long time; to hand such major expenses as children, college costs and weddings; to buy cars and homes; to afford a comfortable retirement; to protect against long-term care costs; and to pass wealth to your heirs--that you need to create a financial plan.--Ric Edelman, The Truth About Money

Part I of The Truth About Money, "Introduction to Financial Planning," discusses the reasons one needs and wants money. Chapter 1 then lists "The Four Obstacles to Building Wealth": procrastination, spending habits, inflation, and taxes.

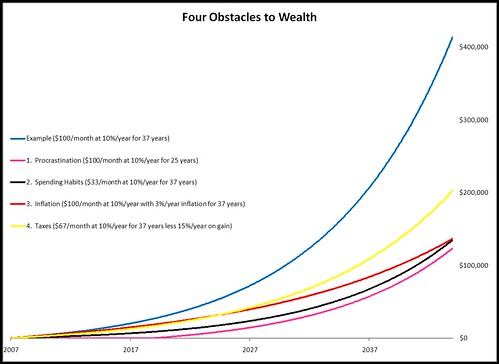

Imagine a raise of $100 per month invested in stocks producing a combined 10% return. As Kiyosaki writes, buy an asset the produces portfolio income. Investing $100 per month from age 28 to age 65 (e.g., now until 2044) would be a total investment of $44,400. Compounding would make the investment worth almost $414,000.

This scenario enables calculating an example of the four obstacles Ric Edelman lists:

- First, reducing the years of contribution from 37 to 25 (e.g., now until 2032) illustrates the effects of procrastination. If the same investment begins at age 40 instead of age 28, the total contributions decrease to $30,000, while the investment value at age 65 decreases to a little more than $123,000. This is almost $291,000 less than original scenario!

- Imagine celebrating the raise by buying a Starbucks Grande Caffè Mocha on the way to work each day, except two vacation weeks. This spending habit could reduce the $100 raise by about $67, leaving $33 per month for investment. At age 65 there would be almost $135,000, or $279,000 less than the original scenario.

- The preceding examples ignore inflation. If inflation were nominally 3% per year, $1.00 at age 28 would buy as much as $3.03 at age 65. So the $414,000 at age 65 would only buy as much as $137,000 did at age 28. Inflation would remove more than $277,000 of purchasing power.

- Finally, consider taxes. A $100 raise could have a marginal tax rate of 33%. Kiyosaki notes the US government taxes earned income the most. This could reduce contributions to $67 per month, less than $30,000 total. At age 65--ignoring capital gains taxes--there would be almost $279,000. Withdrawing from the investment each year to pay capital gains tax, however, would reduce the value to about $203,000, or about $210,000 less than the original scenario.

- Twelve years of procrastination reduces the value of the sample investment by $291,000.

- A workday mocha spending habit reduces the sample investment by $279,000.

- Three percent inflation reduces the purchasing power of the sample investment by $277,000.

- Income and capital gains taxes could reduce the value of the sample investment by $210,000.

(The remainder of this post explains calculation details: As an example--not an endorsement--, First American Mutual Funds FSKSX had a past performance of approximately 10%. The calculations use 9.569% compounded monthly, with no volatility for simplicity. Each scenario has additional assumptions:

- The future value (37 years * 12 months/year =) 444 months later of a $100 per month annuity at (9.569%/year / 12 months/year = ) 0.7974 % per month is $413,890.79. The future value of the same annuity only (25 years * 12 months/year =) 300 months later is $123,333.15.

- On Capitol Hill, Seattle, 8.9% sales tax makes a $2.95 mocha cost $3.21. Five mocha purchases per week for 50 weeks of the year is an average of 21 mocha purchases per month. The average cost is then $67.41 per month.

- The inflation calculation assumes 0.25% per month, which is similar to current values but low considering long-term averages. The present value of a future sum of $413,890.79 at a rate of 0.25% per month for 444 months is $136,590.49.

- A "regular" employee who earns $30,651 to $74,200 per year in Washington state would have no state income tax, but would pay 25% United States income tax plus 6.2% for Social Security plus 1.45% for Medicare. For that tax bracket capital gains taxes are 15%. The calculation assumes this applies to all the gains, which is the worst-case scenario--but still has less effect than the spending habit or procrastination example.)

No comments:

Post a Comment