Many people fail to save because they simply don't want to stop spending. Fine. Keep spending. In fact, I want you to.--Ric Edelman, The Truth About Money

Just change what you spend your money on:

Instead of buying a bottle of ketchup, buy Heinz stock.

Like Kiyosaki, Edelman writes, "instead of buying things that later will have no value (like an empty ketchup bottle or a vacation), or virtually no value (like costume jewelry, clothing, or furniture), make sure the things you buy will retain and even grow in value." What are these things? Unlike a bottle of ketchup, there's no grocery store for investments. Parts 2 through 5 of The Truth About Money explain things that retain or grow in value, with many examples, graphs, and stories. (The cover is right that it's "personal finance that's fun to read!") This grocery store of investments has aisles for cash equivalents, income-producing investments, growth investments, and packaged products:

- Cash Equivalents have little or no default risk. They can mature in more than one year--e.g., some bank certificates of deposit or commercial paper, U.S. EE Savings Bonds, U.S. Treasury Notes, and U.S. Treasury Bonds--or less than one year--e.g., checking accounts, savings accounts, money market funds, some certificates of deposit, and U.S. Treasury Bills. Ric recommends having six to twelve months' expenses available in less than one year, but otherwise avoiding cash equivalents because inflation erases their returns. Some cash equivalents have surrender charges and tax penalties--e.g., life insurance cash value or fixed annuities. These are not appropriate for cash reserves.

- Income-producing investments are subject to default risk (indicated by the bond rating), event risk, and interest rate risk--which one can reduce by holding to maturity or hedging (e.g., with gold). Ric recommends favoring total return rather than rate or even yield. The Truth About Money discusses these income-producing investments:

- U.S. Government Securities include--in addition to cash equivalents--Ginnie Mae, Fannie Mae, Sallie Mae, and Freddie Mac. A GNMA repays principal as well as interest, and can prepay in 12-15 years instead 30 years.

- Municipal Bonds may be (currently) income-tax-free, but Ric disputes the relevance of this--and the wisdom of insuring them. In addition, municipal bonds are often callable.

- Ric recommends against Zero Coupon Bonds because they give low returns, lack payment before possible default, incur taxes on phantom income, and are callable. He also discourages taking physical possession of their certificates.

- Investments that confer ownership or equity instead of (or in addition to) income rely on growth for their value. The Truth About Money discusses these growth investments:

- Stocks grow in value, generate income, have returns that beat inflation, and have tax advantages (tax on capital gains is less than the tax on income or interest, tax isn't due until sale, and heirs don't pay capital gains tax). One can purchase stocks through brokerage firms, discount brokers, or dividend reinvestment plans. Although buying international stock adds currency risk exposure, Ric observes that the international stocks and companies are increasing in value.

- Real Estate investing adds diversity--but also hassle. For real estate investment Ric recommends lots of cash, for reserves and purchases.

- Collectibles don't make good investments due to the possibility of fraud or damage, and inability or unwillingness to sell.

- Hedge Positions could help insure against inflation (e.g., gold), deflation (e.g., bonds, dividend-paying stocks, and cash), recession (e.g., oil and gas, minerals, forest products), lack of confidence (e.g., real estate, gold, and precious metals), collapse of the dollar (e.g., foreign stocks and currencies), and stock market crash (e.g., selling short or options trading like covered call writing).

- Just as a real grocery store has prepared foods, the investment grocery store has packaged products--which are really investment companies. These make investments affordable, liquid, diversified, and professionally managed. Open-end or mutual funds have an annual expense ratio and a sales charge (front-end load, back-end load, level load, or no-load). The Truth About Money discusses these packaged products, beginning with six mutual fund types:

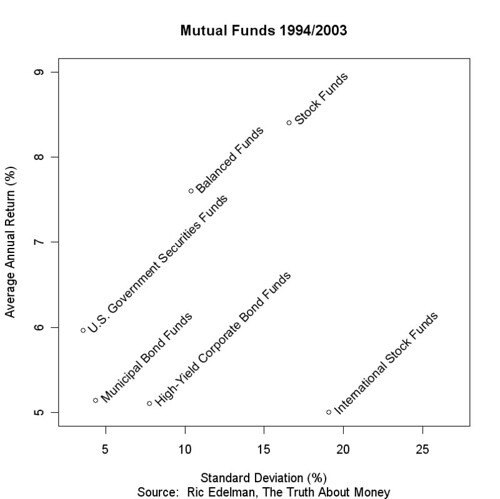

- U.S. Government Securities Funds exist, despite the perception that mutual funds are mostly a method to invest in stocks. These include Ginnie Mae funds, zero-coupon funds, intermediate funds, short-term funds, and ultra-short funds. Related funds are adjustable rate mortgage funds and global government funds.

- Municipal Bond Funds include money market funds, single-state funds (to avoid state income tax), Puerto Rico funds (to avoid all income taxes), insured muni funds, and high-yield muni funds.

- High-Yield Corporate Bond Funds (in contrast with short-term and intermediate funds) invest in long-term speculative grade bonds. Investors thus face credit risk in addition to interest rate risk.

- Balanced Funds invest in four asset classes: cash and cash equivalents, government securities, corporate bonds, and corporate stocks. There are related fund types: Asset Allocation Funds add other asset classes, Growth and Income funds limit asset classes to stock and bonds only, and Equity Income invest in stocks which pay dividends.

- Stock Funds can focus on different categories of market capitalization, different sectors, or different indexes.

- International Funds are open-end or mutual funds available in a variety of types: global funds, international funds, single nation funds, regional funds, or sector funds.

- Closed-End Funds, while still investment companies, differ from open-end or mutual funds. Shares generally trade on a stock exchange rather directly with the fund.

- Unit Investment Trusts are the third type of investment company different from open-end or closed-end funds. They have a fixed portfolio and definite maturity date.

- Wrap Accounts are not investment companies but accounts that protect investors from unnecessary trading commissions. However, Ric lists "11 Reasons to Avoid Wrap Accounts."

- Annuities are available from insurance companies. Variable annuities are securities products, however. They provide tax-deferred growth and guarantees against loss (in the form of living benefits and death benefits) at the cost of fees similar to mutual funds, plus contract fees and mortality charges.

- Real Estate Limited Partnerships are companies that permit investing in real estate with less hassle (for the limited partners). The Tax Reform Act of 1986 retroactively classified their income as passive, so investors cannot deduct losses from active income.

- Real Estate Investment Trusts (REIT) are like Real Estate Limited Partnerships, except that they are publicly traded.

No comments:

Post a Comment